Financing

21st Mortgage Financing

Application

Visit the 21st Mortgage site to submit an application.

They will ask who you are buying it from. Select "Manufactured home Dealer."

Nelson Homes dealer number is

243 1.

Please put that in the application when asked.

NOTE. It will ask you for sales tax. Don't enter anything there. There may or may not be any sales tax.

Two Basic Types Of Loans for used or new home purchases.

- Home only Loans where the land is not included in financing.

- Land with home where the purchase, or using the land as collateral.

Here is some information about 21st Mortgage:

- You don't have to have a specific home to apply. You can just pick one off my site or you can make one up. You can put in any location that you want (Park, own land, etc). The home is not pertinent in the beginning. There are different interest rates if the home is new or used less than 10 years old, and more than 10 years old. Try to get the year right.

- They will finance moving of the home into the loan on a used home. This is huge. No out-of-pocket money for the move other than the percentage down that they require.

- They will finance land, sewer, water, garages, etc. into the loan package. Construction Loan is automatically included if needed.

- Down payment according to your credit scores. (This is my estimate. They do not tell us what their criteria is.)

- 0 to 20% down payment loans based on your credit score. More down payment will result in lower interest rates and monthly payments. They will tell you the interest rate in the approval letter.

- 0% down loan available to very high credit score customers. (725 or above)

- Up to 30 year terms available. They will generally go long enough to have "low payments."

- Find out answer in 24 hours or less. If you don't qualify for the down payment that you applied for, they will turn you down. They will suggest that you re-apply with a suggested amount down. Call me. I can submit a "re-look with the suggested down payment. They will then send an approval letter.

- Usually they will approve with some larger down payment for substandard credit scores (below 600)

- Co-signer can help with a no credit customer. Generally a younger adult (child)

- Co-signer cannot help with a customer with substandard credit.

- You can buy for a person with 20% down payment. This is for someone who has a child, parent etc that would not quality. I have had a person from another state buy a home for their parent. You don't have to be a local to do the buy for.

- National finance company in 48 states. Owned by Berkshire Hathaway (Warren Buffet). They are by far the largest lender of manufactured homes in the country.

I would recommend that you apply if you have an interest. There is no cost. If there is a home that is similar to a home that you would be interested in, use that home. If used, add in for moving costs if appropriate. For example, the used home is $50,000 plus an estimate of $10,000 moving, ask for the loan amount of $60,000. We can easily change the home with what they call a "re-look". When you apply, you will find out what your payments, down payment and interest rate would be.

Payment Estimator

Do you want to estimate your payment before you apply? It is easy. Simply visit the Payment Estimator. Just answer some easy prompts about you, the home, who you are buying it from, general location, whether you are financing just the home or land and improvements, and your estimated credit score.

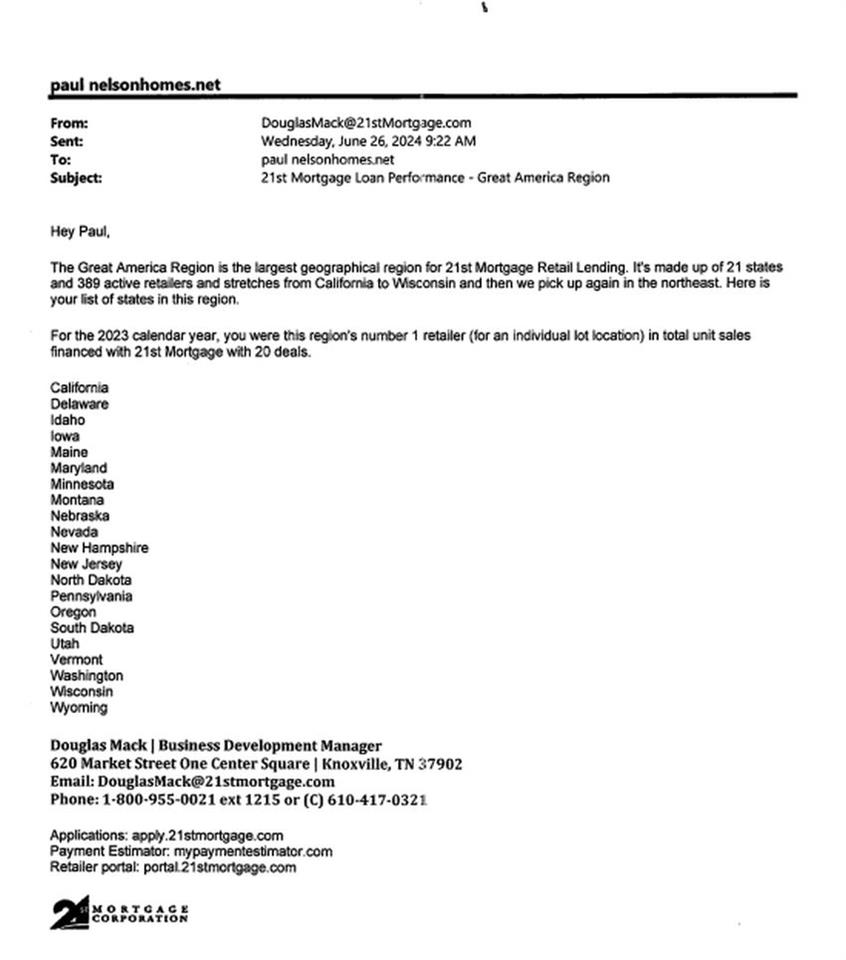

NELSON HOMES WAS 21ST MORTGAGE #1 INDIVIDUAL DEALER IN 21 STATES IN 2023

Below is an email from 21st Mortgage that I was the #1 SINGLE LOCATION in the Great American Region for 21st Mortgage (21 States). I am pretty proud of that. A little dealer from ND is the #1 individual dealer for the largest lender of manufactured homes for almost half the country. People ask me if I recommend 21st Mortgage. I don't recommend anybody. I encourage to shop for financing like they shop for the home. What I do like about 21st Mortgage is that you get a quick "YES" so you can move ahead with your plans. There is no requirement that you use them.